Backtest

Objectives:

- Optimal Rebalance Frequency: Identify the ideal rebalance intervals to maintain portfolio stability and maximize returns while adapting to market changes.

- Improved Return Potential: Ensure that holding the index token delivers consistent, optimized returns through a diversified and dynamically managed portfolio.

- Security Assurance: Enhance investment security by integrating regular security audits and compliance checks, safeguarding user assets from potential risks.

- Regulatory Compliance: Validate that all assets within the indexes adhere to strict regulatory standards, ensuring trust and transparency for investors.

Methods:

- Historical data of component tokens from January 2023 to August 2024 was sourced from rwa.xyz.

- A rebalancing strategy was implemented with a 30% maximum cap and a 2% minimum threshold.

- Price fluctuations over the specified period were analyzed to determine changes in value and calculate profit and loss.

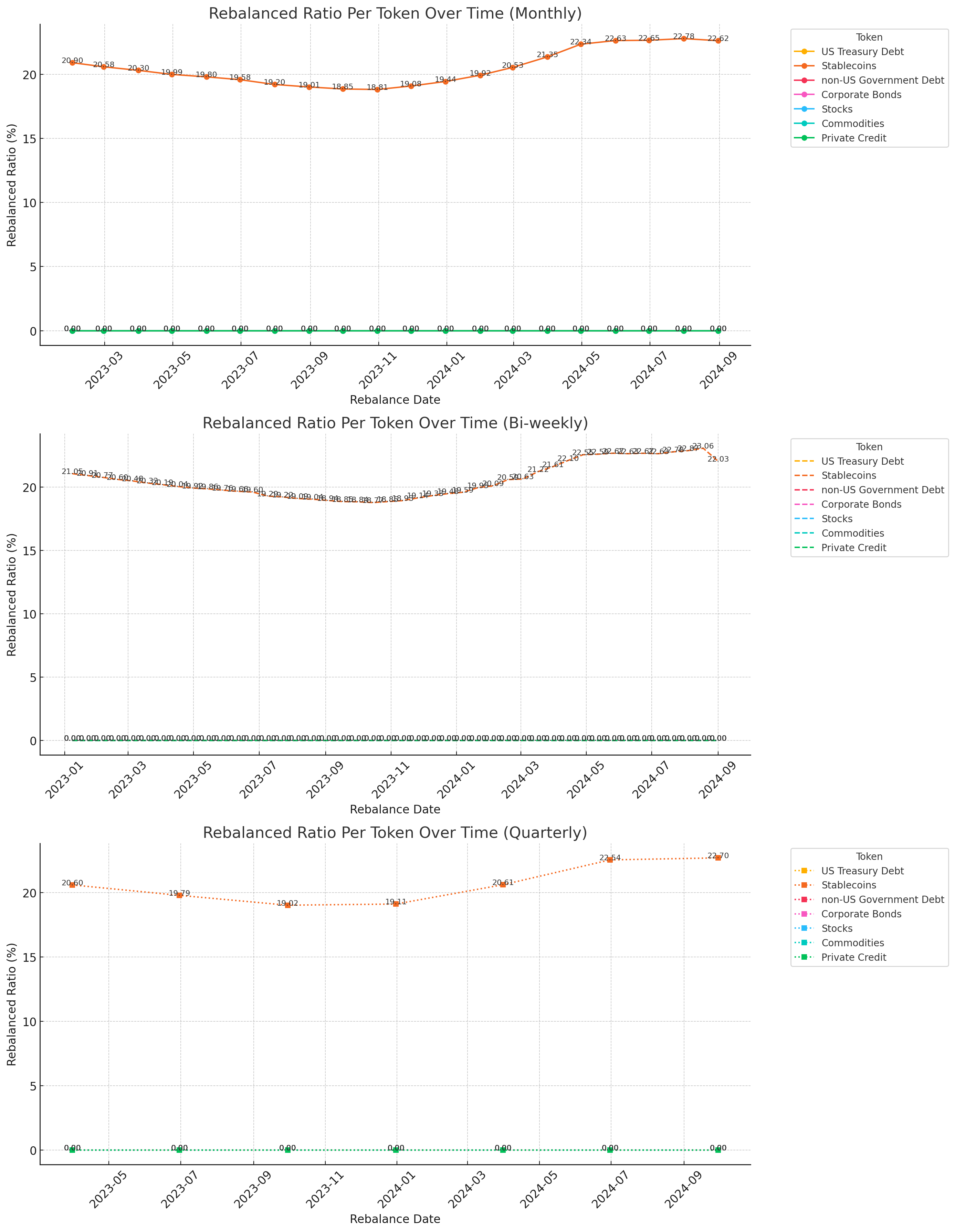

Rebalancing Frequencies: Quarterly, Monthly, Bi-weekly

Given the volatility in the prices of component tokens, rebalancing plays a crucial role in maintaining a stable and diversified portfolio. Our strategy utilizes historical data from January 2023 to August 2024, applying a maximum allocation cap of 30% and a low threshold of 2%. These parameters ensure that each token's influence is balanced, preventing any single asset from skewing the index.

As illustrated in the graphs, bi-weekly rebalancing effectively manages fluctuations, particularly for dominant assets like US Treasury Debt, which remained within a narrow variance range. This method carefully redistributes any excess weight, promoting a well-diversified allocation across the index.

While the analysis highlights that both monthly and quarterly rebalancing offer stability, quarterly rebalancing emerges as the most efficient approach. It provides a balanced trade-off, minimizing the costs associated with more frequent adjustments while maintaining the portfolio’s integrity and performance.